Accounting rate of return method

If you have already studied other capital budgeting methods (net present value method, internal rate of return method and payback method), you may have noticed that all these methods focus on cash flows. But accounting rate of return (ARR) method uses expected net operating income to be generated by the investment proposal rather than focusing on cash flows to evaluate an investment proposal.

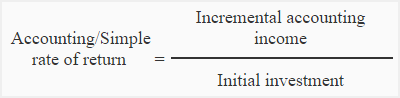

Under this method, the asset’s expected accounting rate of return (ARR) is computed by dividing the expected incremental net operating income by the initial investment and then compared to the management’s desired rate of return to accept or reject a proposal. If the asset’s expected accounting rate of return is greater than or equal to the management’s desired rate of return, the proposal is accepted. Otherwise, it is rejected. The accounting rate of return is computed using the following formula:

Formula of accounting rate of return (ARR):

In the above formula, the incremental net operating income is equal to incremental revenues to be generated by the asset less incremental operating expenses. The incremental operating expenses also include depreciation of the asset.

The denominator in the formula is the amount of investment initially required to purchase the asset. If an old asset is replaced with a new one, the amount of initial investment would be reduced by any proceeds realized from the sale of old equipment.

Example

The Fine Clothing Factory wants to replace an old machine with a new one. The old machine can be sold to a small factory for $10,000. The new machine would increase annual revenue by $150,000 and annual operating expenses by $60,000. The new machine would cost $360,000. The estimated useful life of the machine is 12 years with zero salvage value.

Required:

- Compute accounting rate of return (ARR) of the machine using above information.

- Should Fine Clothing Factory purchase the machine if management wants an accounting rate of return of 15% on all capital investments?

Solution:

(1): Computation of accounting rate of return:

= $60,000* / $350,000**

= 17.14%

*Incremental net operating income:

Incremental revenues – Incremental expenses including depreciation

$150,000 – ($60,000 cash operating expenses + $30,000 depreciation)

$150,000 – $90,000

$60,000

** The amount of initial investment has been reduced by the net realizable value of the old machine ($360,000 – $10,000).

(2). Conclusion:

According to accounting rate of return method, the Fine Clothing Factory should purchases the machine because its estimated accounting rate of return is 17.14% which is greater than the management’s desired rate of return of 15%.

Cost reduction projects:

The accounting rate of return method is equally beneficial to evaluate cost reduction projects. The accounting rate of return of the assets that are purchased with a view to reduce business costs is computed using the following formula:

Example

The P & G company is considering to purchase an equipment costing $45,000 to be used in packing department. It would reduce annual labor cost by $12,000. The useful life of the equipment would be 15 years with no salvage value. The operating expenses of the equipment other than depreciation would be $3,000 per year.

Required: Compute accounting rate of return/simple rate of return of the equipment.

Solution:

= $6,000* / $45,000

= 13.33%

*Net cost savings:

$12,000 – ($3,000 cash operating expenses + $3,000 depreciation expenses)

$12,000 – $6,000

$6,000

Comparison of different alternatives:

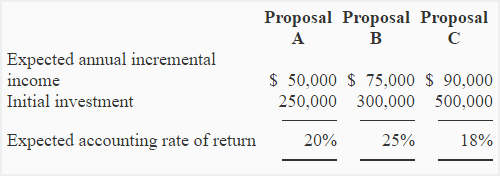

If several proposals are being considered and the management have to choose the best one due to the availability of limited funds, the proposal with the highest accounting rate of return (ARR) is preferred. Let’s compare three projects in the following example:

Example

The Good Year manufacturing company has the following different alternative investment proposals:

Required: Using accounting rate of return method, select the best investment proposal for the company.

Solution

If only accounting rate of return is considered, the proposal B is the best proposal for Good Year manufacturing company because its expected accounting rate of return is the highest among three proposals.

Advantages and disadvantages:

Advantages:

- Accounting rate of return is simple and straightforward to compute.

- It focuses on accounting net operating income. Creditors and investors use accounting net operating income to evaluate the performance of management.

Disadvantages:

- Accounting rate of return method does not take into account the time value of money. Under this method a dollar in hand and a dollar to be received in future are considered of equal value.

- Cash is very important for every business. If an investment quickly generates cash inflow, the company can invest in other profitable projects. But accounting rate of return method focus on accounting net operating income rather than cash flow.

- The accounting rate of return does not remain constant over useful life for many projects. A project may, therefore, look desirable in one period but undesirable in another period.

Leave a comment