Valuation of closing stock on consignment

Content:

- Definition and explanation

- Valuation of closing stock

- Formula and format for computing the value of closing stock on consignment

- Example 1 – valuation using cost price

- Example 2 – valuation using net realizable value (NRV)

Definition and explanation

A consignor may have some incomplete consignments at the end of his accounting year. An incomplete consignment means that there are some unsold units of goods with the consignee when the accounting period of the consignor comes to an end. These unsold units are termed as closing stock on consignment (or just stock on consignment for short) and need to be properly valued. After valuation, the stock on consignment must be brought into the books and credited to the consignment account so that the profit earned on consignment during the period can be computed correctly. The journal entry for this purpose is given below:

Stock on consignment A/C [Dr]

Consignment A/C [Cr]

The stock on consignment is an asset and is, therefore, shown on the year end balance sheet. In the next accounting period when consignment account is prepared, this stock appears as the first item on the debit side of this account. The following journal entry is made for this purpose:

Consignment A/C [Dr]

Stock on consignment A/C [Cr]

Valuation of stock on consignment

The stock on consignment, like in many other business situations, should be valued using lower of cost or market price principle. The major issue in this regard is the ascertainment of cost price and market price of goods in stock. The rest of this article talks about the procedures of determining these two prices. Let’s start with the cost price.

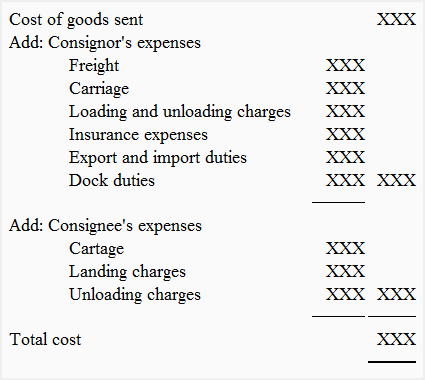

Cost price

The total cost of goods is equal to the expenditures incurred by consignor to bring the goods in salable condition plus all the expenditures paid by consignor as well as consignee in the course of transferring those goods to the consignee’s place. These expenditures usually include carriage, freight, insurance, import and export duties, loading and unloading expenses etc. These expenditures are popularly referred to as non-recurring expenditures.

Any expenditures incurred after the goods have reached to the consignee’s place should be ignored for the purpose of computing the value of closing stock on consignment. Usual examples of such expenditures include warehouse rent, warehouse insurance, storage expenses, carriage paid for the delivery of goods to customers, marketing expenses or any other payment made for the sale of goods.

Net realizable value (NRV)/market price

Net realizable value (NRV) of stock is determined by deducting from the market price of stock the possible expenses required to complete the sale of stock including consignee’s commission. Suppose, for example, 100 units of product X are in stock with a consignee and the sales price of one unit of product is $20. The total sales or market price of this stock would be $2,000 (= 100 units × $20). Now if the estimated expenses required to sell this stock are $300 and consignee’s commission on sale is $200, the net realizable value of stock would be $2,000 (= $2,500 – $500).

After computing the cost price and net realizable value (NRV) in accordance with the procedures explained above, the smaller one should be used as the value of closing stock. If no indication regarding the market price or net realizable value is available in an examination problem or a homework assignment, the students should assume that the cost price is lower than the net realizable value. The valuation of stock on consignment should therefore be done on the basis of cost price.

Formula and format for computing closing stock on consignment

For cost price

If cost price method is applicable, the students should follow the following format for computing the value of closing stock:

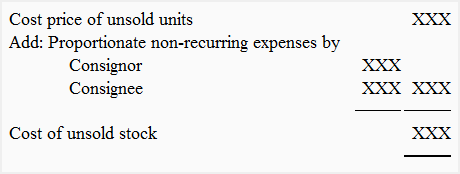

After computing the total cost using above format, the following formula can be used to find the value of stock on consignment:

Cost of stock on consignment = (Total cost/Total number of units) × Units in stock

Alternatively, the value of stock can also be computed as follows:

For net realizable value (NRV)

If net realizable value method is applicable, the following formula should be used to compute the value of stock on consignment.

Net realizable value = Market price of stock – (Expected expenses to be incurred to sell the stock including consignee’s commission)

Example 1 – valuation using cost price

This example illustrates a situation where we need to take the cost of stock as the value of closing stock on consignment.

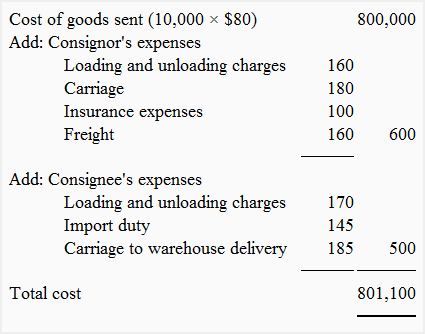

On June 1, 2020, Robert & Co. of Mexico consigned 10,000 units of goods to Peter & Co. of Ottawa at a cost of $80 per unit. Robert & Co. paid the following expenses:

- Loading and unloading charges: $160

- Carriage: $180

- Insurance: $100

- Freight: $150

The following expenses were paid by Peter & Co. on behalf of Robert & Co:

- Loading and unloading charges: $170

- Import duty: $135

- Carriage for delivering goods to consignee’s warehouse: $185

- Selling and marketing expenses: $110

- Warehouse rent: $125

The consignee’s commission was 5% on gross sale proceeds

On December 31, 2020, Peter & Co. sent an account sales to Robert & Co. sowing that 8,000 units were sold at a price of $110 per unit and 2,000 units remained unsold. The Robert & Co. prepares its profit and loss account and balance sheet on December 31 each year.

Required: Compute the value of closing stock on consignment on December 31, 2020.

Solution

Valuation of closing stock on consignment

Stock on consignment = ($801,100/10,000 units) × 2,000 units

= $160,220

Note: The selling and marketing expenses of $110 and warehouse rent of $125 paid by consignee have not been taken into account while determining the value of stock on consignment because these two expenses have been incurred after the goods have reached to the consignee’s place or warehouse.

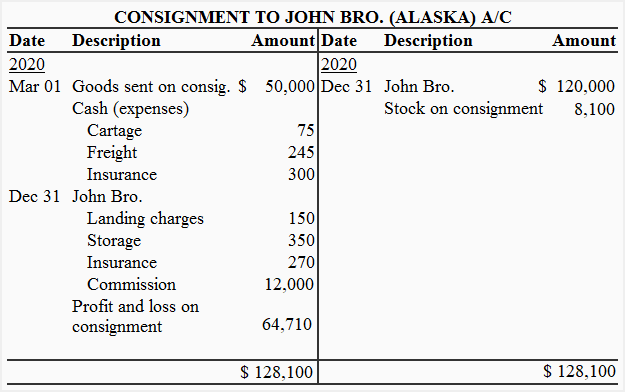

Example 2 – valuation using net realizable value

This example illustrates a situation where we need to take the net realizable value of stock as the value of closing stock on consignment.

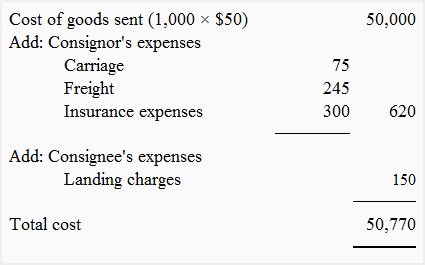

On March 1, 2019, David Bro. of Mumbai shipped to John Bro. of Alaska 1,000 units of a hunting tool costing $50 each. David Bro. incurred the following expenses for this shipment:

- Cartage: $75

- Freight: $250

- Insurance: $300

The following charges were paid by John Bro:

- Landing charges: $150

- Storage charges: $350

- Fire insurance premium on stock: $270

On December 31, 2019, an account sales was received from John Bro. revealing that 800 units were sold at $150 each.

Suddenly a new hunting tool appeared in the market towards the close of the year and it became impossible to sell the remaining 200 units at high price. The market price of the tool fell down to $45 per unit. The john bro. deducted all the expenses they paid in connection with the consignment and also charged a commission at an agreed rate of 10% on total gross sale proceeds.

A bank draft for the balance due was attached with the account sales.

Required:

- Find out the value of closing stock on consignment.

- Prepare a journal entry to bring the stock on consignment into books of David Bro.

- Prepare consignment to john account in the books of David Bro.

Solution:

1. Valuation of stock on consignment:

(i). Stock on consignment = ($50,770/1,000 units) × 200 units

= $10,154

(ii). Market price of stock – Expected expenses to sell the stock

= (200 units × $45) – $900*

= $9,000 – $900

= $8,100

*Expected expenses to sell the stock consist of only consignee’s commission as no other information in this regard is available. Consignee’s commission is: $900 (= $9,000 × 10%).

The net realizable value of stock ($8,100) is less than its cost ($10,154). The value of closing stock on consignment is, therefore, $8,100.

Note: The storage charges of $350 and fire insurance premium of $270 paid by consignee have not been taken into account while determining the value of stock on consignment because these two expenses have been incurred after the goods have reached to the consignee’s place or warehouse.

2. Journal entry

3. Consignment to John account

Consignee’s commission on gross sales: $120,000 × 10% = $12,000

Really appreciated