Consignment account

Consignment account is prepared to ascertain the profit earned or loss incurred by the consignor on a specific consignment. This account can be viewed as a combined trading and profit and loss account prepared specifically for consignment business.

The nature of the consignment account is nominal which means it is drawn up to show the results of the consignment business for a specific period.

If consignor sends goods to more than one consignees working in different cities or areas, a separate consignment account is required for each consignment so that the profit or loss for each consignment can be determined separately. If consignor maintains more than one consignment accounts, he can distinguish them from each other by adding to the account title the name of the consignee or the name of the city or area to which the particular consignment belongs. For example, Consignment to David, Consignment to John, Consignment to Ottawa and consignment to New York etc.

Debit and credit entries in a consignment account

The entries in the consignment account are made on the basis of consignor’s own record as well as account sales sent by the consignee. The debit and credit entries are made as follows:

Debit entries

The common entries that appear on the debit side of a consignment account are listed below:

- Opening stock of goods (if any)

- Total cost of goods sent on consignment

- All the expenses incurred by consignor such as loading, freight, insurance etc.

- All the expenses paid by consignee such as unloading, freight, godwon rent, warehousing and storage, marketing expenses, packaging and selling expense etc.

- Bad debts regarding consignment sales.

- Consignee’s ordinary and del credere commission at agreed rate on sale proceeds.

Credit entries

The usual items that appear on the credit side of a consignment account are listed below:

- Gross sale proceeds

- Closing stock of goods (if any)

- Abnormal loss of goods

- Stock in transit (if any)

The balance of consignment account represents a profit or a loss on consignment and is transferred to “Profit and Loss on Consignment Account“. The consignment account is thus closed.

The Profit and Loss on Consignment Account is also a nominal account. If there are more than one consignments, the balances of all consignment accounts are transferred to this account.

The profit and loss on consignment account is closed at the end of the year by transferring its balance to the “General Profit and Loss Account“.

Format and example

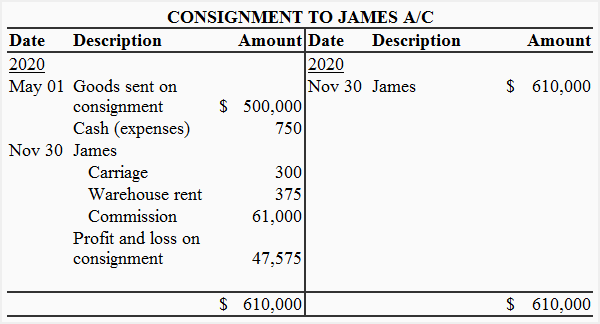

Example 1

In this example, consignor sends goods to Mr. James who is located in Ontario city. The consignee’s name in account title distinguishes this consignment account from others.

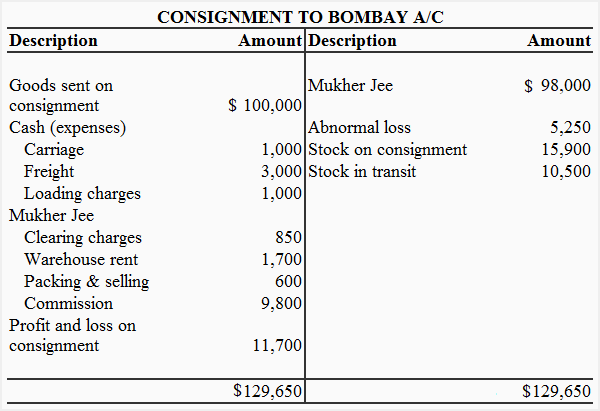

Example 2

This consignment is sent to Mukher Jee in Bombay city. The city name included in the account title distinguishes it from other consignments.

It was very helpful

It is simplified and gives insight to understanding of the topic.