Stock split

As companies grow, their per share market price usually increases, and sometimes it becomes too expensive or even unaffordable for the common investor. In such situations, companies usually use a device known as a stock split to lower the market price of their stock so that it becomes more affordable and looks more appealing to a greater number of investors.

Content:

- Definition and explanation

- How does stock split affect the market price?

- Accounting/Journal entry

- Example

- Reverse stock split

- Example of reverse stock split

Definition and explanation

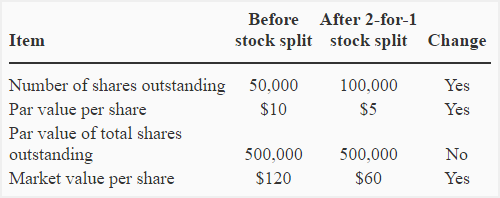

Stock split (sometimes referred to as forward stock split) is a practice of increasing the total number of shares of common stock outstanding and making a proportional decrease in the per share par value so that the aggregate amount of all outstanding shares remains unchanged. Suppose, for example, David Inc. currently has 50,000 shares of $10 par value common stock outstanding and decides a 2-for-1 stock split. After this, the Inc. will have 100,000 shares of $5 par value common stock outstanding but the total par value of shares will remain the same as before the split. A stockholder who currently owns 100 shares of $10 par value each will own 200 shares of $5 par value each after 2-for-1 stock split.

How does stock split affect the market price?

The primary purpose of stock split is to decrease the market price of company’s share so that it becomes more accessible and affordable to potential shareholders and investors. This practice immediately decreases the market price of a company’s stock because the number of shares outstanding are increased without any increase in the value of assets and total stockholders equity. For example, If the current market price of David Inc’s stock is $120 per share, hopefully it will come down to $60 per share immediately after 2-for-1 stock split.

The concept explained so for is summarized below:

A stock split works much similar to a large scale stock dividend in that the distribution of additional shares under both is usually substantial enough to affect the market price of the stock.

Accounting/Journal entry:

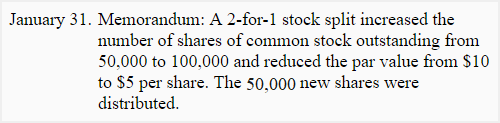

Stock split does not change the balance of any account; it is therefore not recorded by way of a proper double entry. However, it is brought into record just by means of a memorandum entry. The memorandum entry of David Inc. for a 2-for-1 stock split will be made as follows:

Example:

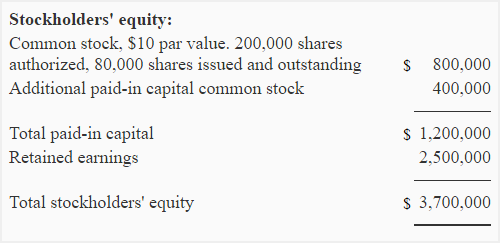

The stock holders’ equity section of the balance sheet of Western Company at December 31, 2020, is given below:

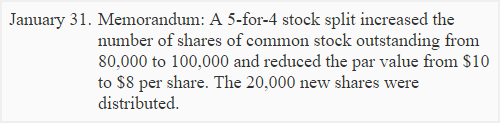

On 31 January 2021, the board of directors proposed a 5-for-4 stock split which was duly approved and new shares were distributed among stockholders.

Required:

- Compute the number of shares that were distributed among stockholders as a result of this 5-for-4 stock split.

- Compute the par value per share after this split.

- What accounting entry will be made for this split?

- Show stockholders’ equity section of the company immediately after 5-for-4 stock split.

Solution:

(1). New shares distributed:

Number of shares before stock split: 80,000 shares

Number of total shares after 5-for-4 stock split: Shareholders holding 4 shares pre-split will hold 5 shares post-split i.e., they will get an additional share for each 4 shares they currently own. Western’s total post-split number of shares have been calculated below:

(80,000/4) × 5 = 100,000 shares

Additional shares distributed among stockholders as a result of 5-for-4 stock split: 100,000 shares – 80,000 shares = 20,000 shares

(2). Par value per share after split:

$800,000/100,000 shares = $8

(3). Accounting/journal entry:

The Western Company will make the following memorandum entry to show the change in number of shares of common stock outstanding and the change in its per share par value:

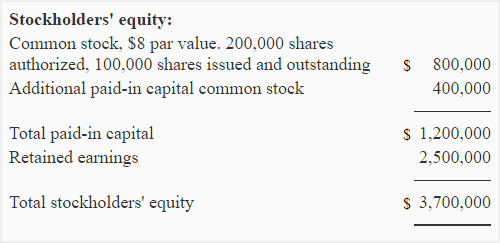

(4). Stockholders equity after 5-for-4 stock split:

Notice that there is no impact on the total par value of common stock and the total stockholders’ equity of Western Company. These two amounts are the same as they were before the execution of this 5-for-4 stock split.

In Real Business – Samsung’s 50-for-1 Stock Split:

Samsung announced a 50-for-1 stock split in May 2018. This announcement was intended to lower the market price of company’s stock which was being traded at 2.65 won (app. $2,467) per share prior to split. Samsung’s split announcement worked as expected and caused the share price to immediately drop to 0.053 won (app. $49) per share. This action slightly dropped the company’s trading activities for a short period of time but attracted a significant number of new investors by making its stock more accessible to general public.

Source: Reuters, May 3, 2018. https://www.reuters.com/article/us-samsung-elec-stocks/samsung-elec-shares-open-at-53000-won-each-after-501-stock-split-idUSKBN1I500B

Reverse stock split

A reverse stock split, as the name implies, is the opposite of a forward or normal stock split. It occurs when a company intends to raise the market price of its share by reducing its total number of outstanding shares available to shareholders. It is executed by merging the existing number of shares to a relatively fewer but proportionally higher par value shares. Hence, the per share par value increases but the total par value of company’s all outstanding shares remains unchanged. For example, a 1-for-2 stock split would be called a reverse stock split because it would reduce the number of outstanding shares to their half and increase the per share par value to double. Consequently, the ultimate par value amount to be reported in the balance sheet will remain unaffected, similar to the forward stock split, explained earlier in this article.

While the companies practically have a very little to no direct control over their stock prices, the desired result of a reverse split is often the increased market price of their common stock. A common factor that drives companies to consider for a reverse stock split is to maintain the minimum share price set by the stock exchange in which they are listed so as to protect themselves from being delisted from the exchange.

Journal entry for reverse stock split

For recording purpose, a reverse stock split does not require a double entry accounting because it does not affect the ultimate reporting amount of any item in stockholders’ equity. Like a forward split, no double entry accounting is needed to book a reverse stock split. The change in the number of shares and their par value resulting from the execution of a reverse split is brought to record by means of just a memorandum entry.

Example of reverse stock split

Arnold, a less experienced investor, owns 1,000 shares of Toronto Inc. at $0.5, the total value being $500. Toronto Inc. currently has 500,000 shares outstanding and it announces a 1-for-10 reverse stock split. Consequently, each 10 shares of common stock currently held by shareholders would be consolidated and converted to 1 share of common stock. How would the Arnold’s investment be affected if Toronto’s announcement for this reverse stock split is successfully executed.

Solution

Step 1: Compute Toronto’s pre-split market capitalization:

500,000 shares x $0.5

= $250,000

Step 2: Compute Toronto’s post-split number of shares:

(500,000/10) x 1

= 50,000 shares

Step 3: Compute Toronto’s post-split per share value:

Since Toronto’s 1-for-10 reverse split would not change its total market capitalization, we can compute the value of each of its share by dividing the pre-split market capitalization by the post-split number of shares, which comes to $5 as computed below:

= $250,000/50,000 shares

= $5 per share

Step 4: Compute Arnold’s post-split investment value:

After Toronto’s execution of this reverse split, Arnold would own 100 shares (= 1,000 shares/10) with a total value of $500 (= 100 shares x $5). Arnold’s total investment value would thus not be affected and remain the same after Toronto’s reverse stock split execution.

Leave a comment