Exercise-6 (Materials, labor and variable overhead variances)

P&G company produces many products for household use. The company sells products to storekeepers as well as to customers. Detergent-DX is one of the products of P&G. It is a cleaning product that is produced, packed in large boxes and then sold to customers and storekeepers.

P&G uses a traditional standard costing system to control costs and has established the following materials, labor and overhead standards to produce one box of Detergent-DX:

- Direct materials – 1.5 pounds @ $12 per pound: $18.00

- Direct labor – 0.6 hours @ $24 per hour: $14.40

- Variable manufacturing overhead – 0.6 hours @ $5.00: $3.00

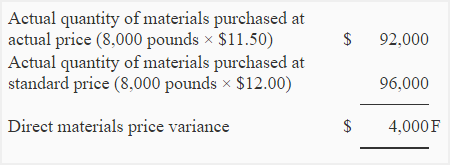

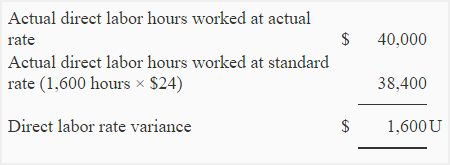

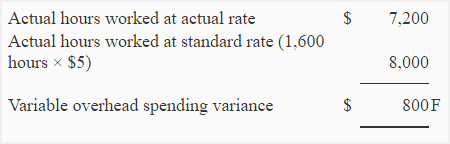

During August 2023, company produced and sold 3,000 boxes of Detergent-DX. 8,000 pounds of direct materials were purchased @ $11.50 per pound. Out of these 8,000 pounds, 6,000 pounds were used during August. There was no inventory at the beginning of August. 1600 direct labor hours were recorded during the month at a cost of $40,000. The variable manufacturing overhead costs during August totaled $7,200.

Required:

- Compute materials price variance and materials quantity variance. Assume that the materials price variance is computed at the time of purchase.

- Compute direct labor rate variance and direct labor efficiency variance.

- Compute variable overhead spending variance and variable overhead efficiency variance.

Solution:

(1). Materials variances:

a. Materials price variance:

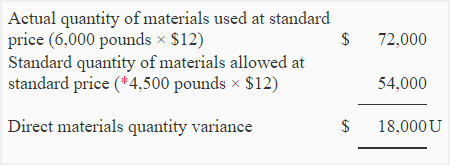

b. Materials quantity variance:

*3,000 boxes × 1.5 pounds per box = 4,500 pounds

F = Favorable

U = Unfavorable

(2). Labor variances:

a. Direct labor rate variance:

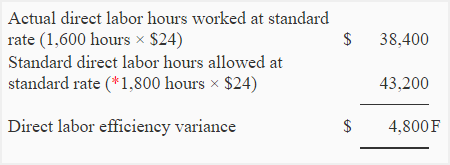

b. Direct labor efficiency variance:

*3,000 boxes × 0.6 hours per box = 1,800 hours

F = Favorable

U = Unfavorable

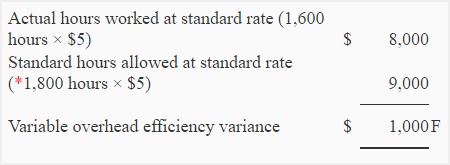

(3) Variable overhead variances:

a. Variable overhead spending variance:

b. Variable overhead efficiency variance:

*3,000 boxes × 0.6 hours per box = 1,800 hours

F = Favorable

Leave a comment