Direct materials price variance

In managerial accounting, variance means deviation of actual costs from standard costs. Materials price variance is the result of deviation of actual price paid for materials from what has been set as standard. Direct materials price and quantity standards are set after keeping in mind the current market prices and anticipated changes in materials prices in near future. However things do not always happen as expected and therefore, the actual price of materials purchased and used may significantly deviate from standard price. Moreover, the expenses associated with the order (like freight, duties, handling expenses etc.) may increase or reduce the ultimate price of materials available for use in a manufacturer’s stock. A business may, therefore, have to pay more or less price than what has been considered as normal at the time of setting standards (see direct materials price and quantity standards article).

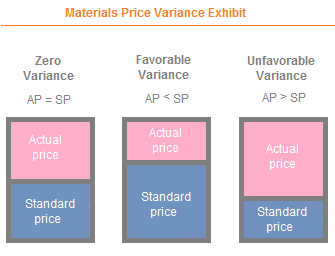

If the actual price paid for materials is more than the standard price, an unfavorable materials price variance occurs. On the other hand, if the actual price paid for the materials is less than the standard price, a favorable materials price variance occurs.

Formula

The formula of direct materials price variance is given below:

Direct materials price variance = (Actual quantity purchased × Actual rate) – (Actual quantity purchased × Standard rate)

Example

The Aptex company manufactures and sells small speakers that are used in mobile phones. The speakers are sold in bulk to mobile manufacturing companies where complete mobiles are produced. The direct material of Aptex company is a thin copper coil. One meter of the copper coil is the standard requirement to manufacture one speaker.

The standard cost to manufacture one speaker is as follows:

Direct materials (1 meter × $1.50 per meter): $1.50

Direct labor: $1.00

Manufacturing overhead: $0.50

During the month of June, 2016, Aptex purchased 5,000 meters of copper coil @ $1.70 per meter and produced 2,500 speakers using 3,000 meters of copper coil.

Required: Calculate direct materials price variance for Aptex company for the month of June, 2016.

Solution:

Direct materials price variance = (Actual quantity purchased × Actual rate) – (Actual quantity purchased × Standard rate)

= (5,000 × $1.70) – (5,000 × $1.50)

= $8,500 – $7,500

= 1,000 Unfavorable

Aptex has an unfavorable materials price variance for June because the actual price paid ($8,500) is more than the standard price allowed ($7,500) for 5,000 meters of copper coil.

This variance can also be computed by using the factored form of above formula:

= AQ × (AR – SR)

= 5,000 meters × ($1.70 – $1.50)

= 5,000 meters × $0.20

= $1,000 Unfavorable

Reasons of direct materials price variance:

A favorable or unfavorable materials price variance may occur due to one or more of the following reasons:

- Order size: Suppliers often allow trade discounts on orders placed in large quantities. The materials purchased in larger quantities can reduce the unit price for buyer and cause a favorable materials price variance for him.

- Rise in price: The rise in the general price level may inflate the input costs of vendors who, as a result, may increase the price of the materials they sell. In an inflationary environment, the frequent rise in the materials prices is among the major causes of unfavorable price variances.

- Urgent needs: If production department does not indicate the need of materials on time, the purchasing department may have to order on urgent basis that may increase the price of materials and other expenses associated with the order.

- Quality: The quality or variety of materials purchased usually have high impact on the cost of materials and may contribute to the occurrence of a favorable or unfavorable price variance. For example, a favorable price variance may be the result of purchasing substandard or low quality materials at lower rates and an unfavorable variance may be the result of purchasing premium or high quality materials at higher rates.

- Inefficient standard setting: Inefficiencies in terms of forecasting and environmental scanning during standard setting process can be a reason of huge price variances.

- Transportation: Transportation can be a significant part of total direct materials cost available in a manufacturer’s stock. The ups and downs in the transportation expenses can impact the total and per unit cost of direct materials available for use and can, therefore, become the reason of a favorable or unfavorable direct materials price variance.

- The role of just in time manufacturing: A company that operates under just in time (JIT) manufacturing system may have to face shortage of direct materials due to a sudden increase in demand for its product. The orders in rush normally cause increased input costs. In such situations, company will have to either accept an unfavorable materials price variance or lost sales.

- Inefficient or unreliable suppliers: A deviation from standard material costs may be the result of ordering with inefficient or unreliable vendors. For example, if suppliers of raw materials are unable to meet the demand, the company may have to look for another supplier. Ordering same materials with multiple suppliers often becomes inconvenient and uneconomical.

Responsibility of direct materials price variance:

Purchasing department is responsible to place orders for direct materials so this variance is generally considered the responsibility of purchase manager. However, the above reasons clarify that the materials price variance may or may not be the result of inefficiencies of the purchasing department.

The occurrence of variances is very normal in both manufacturing and service business. They occur for almost all cost elements and should not be used to find someone to blame. Sometimes they may not be very significant in amount and sometimes they may be the result of factors that are beyond the control of managers. Variances are tools to control costs and improve operating efficiencies They should, therefore, be used positively and in a broader sense.

Leave a comment