Direct materials price and quantity standards

The purpose of setting standards for direct materials is to control direct materials cost. Two types of standards are normally set for direct materials. Theses are materials price standard and materials quantity standard. These two standards are briefly discussed below:

Direct materials price standard:

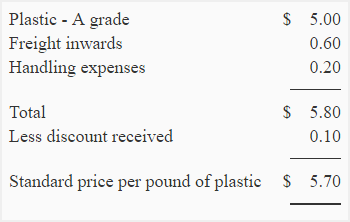

Setting direct materials price standard means determining the expected price of a unit of material. It also includes expenses associated with it i.e., freight, handling charges and octroi duty etc. Every company has different type of expenses associated with materials to get it available for use. If some discount is allowed by the vendor, it is subtracted from the price to arrive at final standard price. For more explanation, consider the following example:

Example:

Super Casing Limited manufactures computer cases which are sold to another company that manufactures complete desktop computers. The Super Casing Limited uses only plastic as direct materials. The standard price per pound of plastic may be calculated as follows:

According to above computations the final standard price of one pound of plastic is $5.70. It means if everything proceeds as planned, the total expenses of a pound of plastic available for use should be $5.70 . But in reality, everything may not happen as expected. The occurrences of deviation from standards are very normal and the common reasons of these deviations are explained on direct materials price variance page.

Direct materials quantity standards:

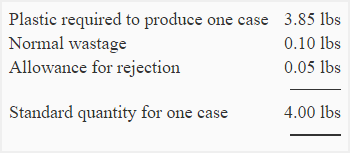

The normal or expected quantity of direct materials required to manufacture a unit of finished product is called standard quantity per unit. It also includes allowances for normal wastage and rejection. In the above example, the standard quantity required to manufacture a single computer case is as follows:

According to above computations, the company requires 4.00 pounds of A grade plastic to manufacture one computer case. But the actual quantity used may be more or less than the quantity allowed by standards. This is quite normal. The reasons of using more or less quantity of direct materials than what has been allowed by standards are discussed on direct materials quantity variance page.

After setting materials price and quantity standards, the standard materials cost for manufacturing one computer case can be calculated using the following equation:

Standard cost of material per unit = Standard quantity to produce one unit × Standard price of materials per unit

= 4.00 lbs. × $5.70

= $22.80

In our example, the standard direct materials cost to manufacture one computer case is $22.80. This standard cost is used to prepare a standard cost card of the product.

Leave a comment