Comprehensive example of job order costing system

The Fine manufacturing company uses job order costing system. The company uses machine hours to apply overhead cost to jobs. At the beginning of 2012, the company estimated that 150,000 machine hours would be worked and $900,000 overhead cost would be incurred during 2012.

The balances of raw materials, work in process (WIP), and finished goods at the beginning of 2012 were as follows:

- Raw materials: $40,000

- Work in process: $30,000

- Finished goods: $60,000

The Fine manufacturing company recorded the following transactions during 2012:

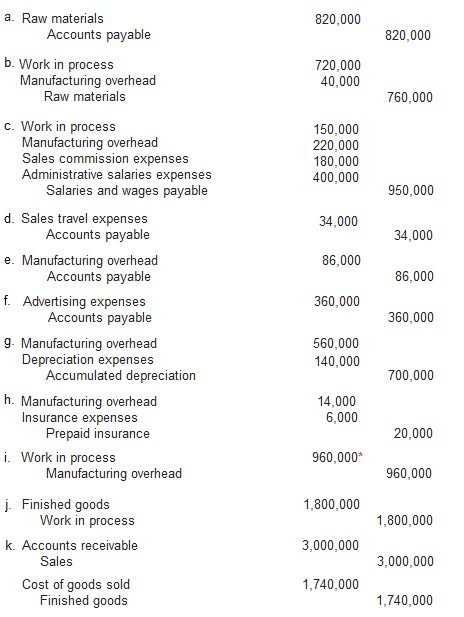

- a. Raw materials purchased on account, $820,000.

- b. Raw materials were requisitioned for use in production, $760,000 ($720,000 direct materials and $40,000 indirect materials).

- c. Direct labor labor, $150,000; indirect labor, $220,000; sales commission, $180,000; and administrative salaries, $400,000.

- d. Sales travel costs were $34,000.

- e. Utility costs incurred in the factory, $86,000.

- f. Advertising expenses were $360,000.

- g. Depreciation for the year was $700,000 ($560,000 relates to factory and $140,000 relates to selling and administrative activities).

- h. Insurance expired during the year, $20,000 ($14,000 relates to factory operations and $6,000 relates to selling and administrative activities).

- i. Fine manufacturing company worked 160,000 machine hours. Manufacturing overhead was applied to production.

- j. Goods costing $1,800,000 were completed during the year.

- k. The goods costing $1,740,000 were sold to customers for $3,000,000.

Required:

- Prepare journal entries, T-accounts and income statement from the above information.

- Prepare a journal entry to close the balance in manufacturing overhead account (over or under applied manufacturing overhead) to cost of goods sold.

Solution:

1 (a). Journal entries:

*Application of manufacturing overhead (entry 9):

Manufacturing overhead is applied to production by multiplying actual direct labor or machine hours worked during the year and predetermined overhead rate computed at the beginning of the year. It is shown as follows:

= $900,000 / 150,000 machine hours

=$6 per machine-hour

Manufacturing overhead applied to production = Actual machine hours × Predetermined overhead rate

= 160,000 hours × $6

$960,000

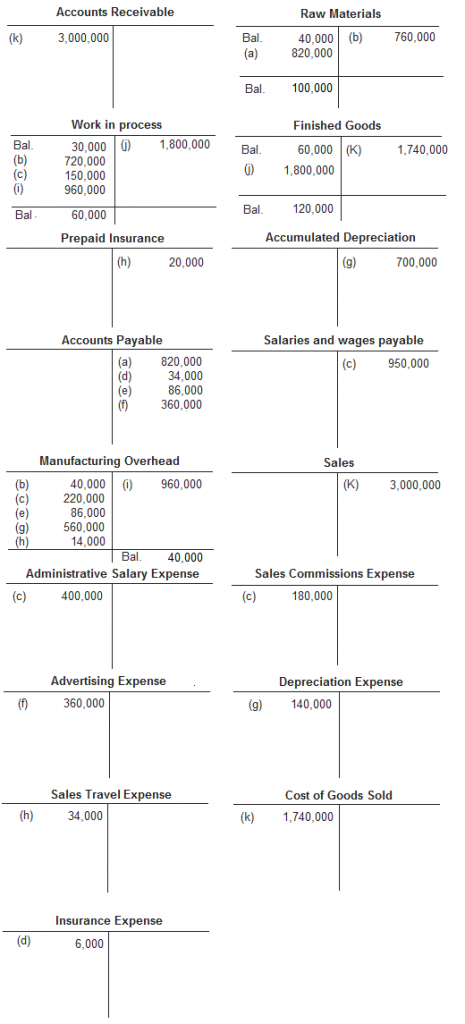

(b) T accounts:

(c) Cost of goods sold statement:

*Over applied manufacturing overhead

2. Journal entry to close the balance in manufacturing overhead account (disposition of over or under applied manufacturing overhead):

Notice that the balance in manufacturing overhead account is credit. It means overhead is over-applied. The following journal entry would dispose it off to cost of goods sold:

| Manufacturing overhead—Dr. | 40,000 | |

| Cost of goods sold–Cr. | 40,000 |

i have problem in COGS statement part c

remarkable learning example