Finished goods and cost of goods sold

Recording finished goods and cost of goods manufactured:

In a job order costing system, all manufacturing costs (i.e., direct materials, direct labor, and applied manufacturing overhead) of the job are debited to work in process account. When a job is completed, its cost (as shown by job cost sheet) is transferred from the work in process account to the finished goods account.

After completion, the job becomes finished goods and is, therefore, transferred from the production department to the finished goods storeroom (also called warehouse).

The following journal entry is made to transfer the cost of a completed job from work in process account to finished goods account:

The total cost transferred from the work in process account to the finished goods account during a period is equal to the cost of goods manufactured for that period.

At the end of a period, the cost of incomplete jobs remain in the work in process account and is shown as “work in process inventory” in assets section of the balance sheet. Next period, this cost represents the opening balance of the work in process account.

Cost of goods sold:

When finished goods are shipped to customers, the cost of finished goods are transferred from finished goods account to cost of goods sold account. If a job is completed according to specification of a particular customer, the complete job is shipped to the customer immediately and the manufacturing cost associated with the job (as shown by the job cost sheet) is charged to the cost of goods sold. But in some cases, the complete job is not shipped but only a portion of the job is sold to customers. In such circumstances, the manufacturing cost per unit is computed and the cost of the units that have been shipped to customers is charged to cost of goods sold account.

Sales and the transfer of cost from finished goods to cost of goods sold account are recorded by making the following journal entries:

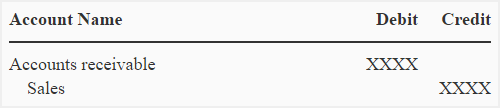

(1). When sales are made:

i. If sales are made on account:

ii. If sales are made on cash

(2). When cost is transferred to cost of goods sold account:

Leave a comment