Periodic inventory system

Explanation

Under periodic inventory system inventory account is not updated for each purchase and each sale. All purchases are debited to purchases account. At the end of the period, the total in purchases account is added to the beginning balance of the inventory to compute cost of goods available for sale. The ending inventory is determined at the end of the period by a physical count and subtracted from the cost of goods available for sale to compute the cost of goods sold.

The general formula to compute cost of goods sold under periodic inventory system is given below:

Cost of goods sold (COGS) = Beginning inventory + Purchases – Closing inventory

Example

The following information belongs to John company, a retailer of high-end fashion products:

- Inventory balance on January 1, 2016: $600,000

- Purchases made during the year 2016: $1,200,000

- Inventory balance on December 31, 2016: $500,000

Required: Compute cost of goods sold for the year 2016 assuming the company uses a periodic inventory system.

Solution:

Cost of goods sold (COGS) = Beginning inventory + Purchases – Closing inventory

= $600,000 + $1,200,000 – $500,000

= $1,300,000

Journal entries in a periodic inventory system:

(1). When goods are purchased from supplier:

(2) When expenses are incurred to obtain goods for sale – freight-in, insurance etc:

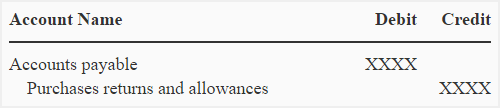

(3). When goods are returned to supplier:

(4). When payment is made to supplier:

(5). When goods are sold to customers:

(6). When goods are returned by customers:

(7). When cash is collected from customers:

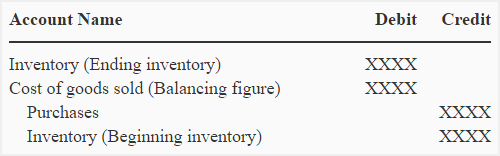

(8). At the end of the period:

Example:

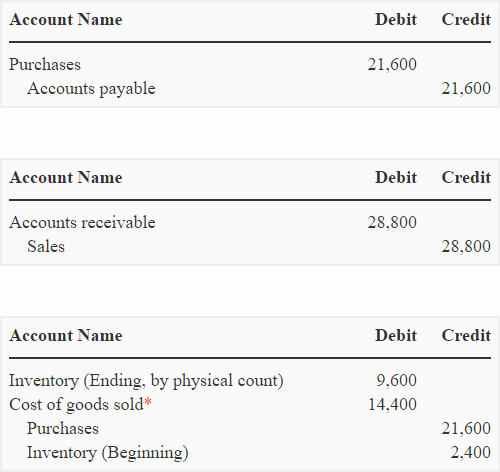

The following information belongs to Paradise Hardware Store:

Beginning inventory: 200 units at $12 = $2,400

Purchases made during the period: 1800 units at $12 = $21,600

Sales made during the period: 1200 units at $24 = $28,800

Ending inventory: 800 units at $12 = $9,600

Required: Make journal entries to record above transactions assuming a periodic inventory system is used by Paradise Hardware Store.

Solution:

* (21,600 + 2,400) – 9,600

Periodic inventory system is usually used by companies that buy and sell a wide variety of inexpensive products.

A disadvantage of periodic inventory system is that overages and shortages of inventory are buried in cost of goods sold because no accounting record is available against which to compare physical count of inventory.

Leave a comment