Sales price variance

Definition and explanation

Sales price variance occurs when actual price at which a product is sold varies from the budgeted or standard price set by the company’s management. It may be defined as the difference between the actual units sold at actual price and the actual units sold at budgeted or standard price.

In other words we can say that the sales price variance is the difference occurred in the amount of sales revenue of a company due to a difference in the actual sales price and the budgeted or standard sales price of a company.

Formula

The sales price variance is computed by using the following simple formulas or equations:

(Actual number of units sold × Actual price) – (Actual number of units sold × Budgeted price)

Or

(Actual price – Budgeted price) × Actual number of units sold

Analysis

The companies set a certain sales price for each product and/or service delivered by them. This price is set based upon the notion that the business will not only cover its costs but also make a reasonable profit. Apart from that the prices of goods or services can also depend on the other factors like the size and age of the business, brand equity, skimming or penetrating pricing strategies, the region or market sector, business norms, product demand and legal restrictions etc.

A business may not always be able to sell all of its goods and services at predetermined or budgeted prices. A deviation of actual price from the budgeted price causes either a favorable or an unfavorable sales price variance. If the actual price at which the products or services of a business actually sold is more than the budgeted price, the sales price variance would be favorable and will result in increased revenues for the business but if the actual sales price is less than the budgeted sales price the sales price variance would be unfavorable and it will result in decreased revenues than expected.

A highly favorable sales price variance achieved from unusually higher prices for goods and services may not be desirable and a signal of higher profitability. Charging unnecessarily higher prices than competitors could have a negative impact on customers’ loyalty which could result in reduced revenue and ultimately reduced profit.

Example 1

MixonTech is an IT company that manufactures mobile phones. It has designed a new model of touch pad mobile phone which it estimates to sell for $500 each in the next year. When the model is introduced in the market, another competitor introduces a new mobile phone model with almost alike features. Due to this Sales Director of MixonTech decides to reduce the price of the mobile phone by $25 so that sales do not get hurt. The company sells a total of 3,000,000 mobile phones but faces a sales prices variance of $75,000,000 as calculated below:

Sales price variance = (Actual Price – Budgeted Price) × Actual units sold

= (*$475 – $500) × 3,000,000 units

= $75,000,000 Unfavorable

*$500 × $25 = $475

Example 2

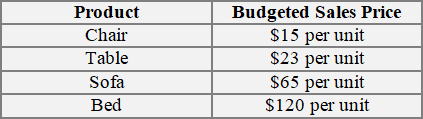

Kim Furniture Mart sells various goods including chairs, tables, sofas and beds. The per unit budgeted prices of these goods are:

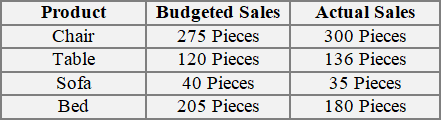

The budgeted and actual sales of these products for the month of September are:

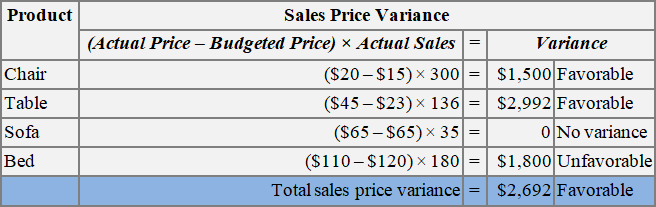

During September, the Kim Furniture Mart found that the costumers were more interested in buying chairs and tables and there was a low demand for beds and sofas. The Mart was unable to sell all the products at their budgeted prices and therefore the manager had to adjust the prices as follows:

Required: For Kim Furniture Mart, compute the sales price variance of each individual product and the sales price variance in total for the month of September.

Solution

Causes of sales price variance

The possible causes of a favorable sales price variance include reduction in competition, better sales price realization, general inflation, sudden increase in demand for the product etc.

The possible causes of unfavorable variance include a tense competition in the industry, introduction of a product by a competitor with similar or better features, reduction in demand for the product, deflation, price caps imposed by governmental regulatory authorities, product obsolescence due to a change in taste and fashion, introduction of an alternative product or solution etc.

Responsibility of sales price variance

The sales department is generally considered responsible for any adverse or unfavorable sales price variance. However, an unfavorable variance may also be the the result of producing poor quality products and improper planning and budgeting etc. In these situations, the responsibility lies on the relevant department rather than the sales department.

Leave a comment