Exercise-12: Sales-to-production-ratio method of joint cost allocation

Posted in: Joint products and by-products (exercises)

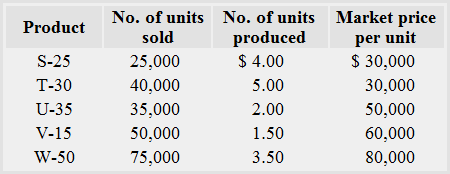

Adolph Inc. produces five products — S-25,T-30,U-35, V-15 and W-50. The joint production cost is $1,000,000 and there is no further processing cost. The demand for Adolph’s products has been fluctuating significantly and production has remained constant.

The information for the past year is provided below:

Required:

- Briefly explain the sales-to-production-ratio method of joint cost allocation.

- Allocate the joint production cost of Adolph Inc. to five products using sales-to-production-ratio method.

Solution

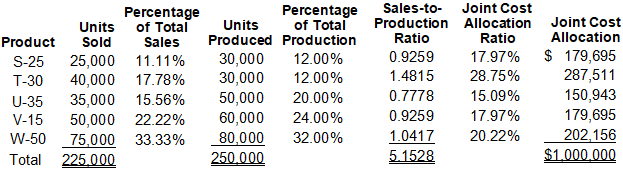

1. About sales-to-production-ratio method:

Under sales-to-production-ratio method, the joint production cost is allocated to different joint products in accordance with a weighting factor which compares the sales percentage with the production percentage. This method allocates a larger share of joint cost to those products that sell the most.

The steps involved in this method are given below:

- Compute the percentage of total sales based on the units of joint product sold.

- Compute the percentage of total production based on the units of joint product produced.

- Compute sales-to-production-ratio using this formula:

Sales-to-production-ratio = Percentage of total sales/percentage of total production - Allocate joint cost by using the sales-to-production-ratio percentage computed in step 3.

2. Allocation of joint cost:

Leave a comment