Accounting for notes receivable

The accounting for notes receivable is simple. When a note is received from a receivable, it is recorded with the face value of the note by making the following journal entry:

A note receivable earns interest revenue for the holder. This revenue is recorded by making the following journal entry:

When the face value as well as interest thereon is collected, the following entry is passed:

Example:

On October 1, 2014, the Western company received a 120 day, 5% note from Southern company in the settlement of an account of $45,000. The Western company collected the note at maturity. The company makes adjusting entries only at the end of the year.

Required: Prepare journal entries to record the acquisition of the note, recognition of interest revenue and the collection of the note at due date.

(1). Acquisition of note:

(2). Recognition of interest revenue:

*(4,5000 × .05) × 3/12 = 562.5

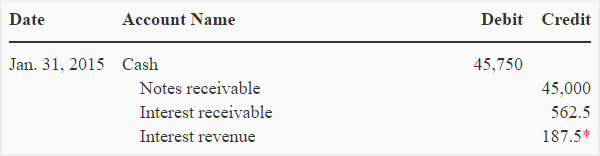

(3). Collection of note:

*(4,5000 × .05) × 1/12 = 187.5

When maker of the note defaults:

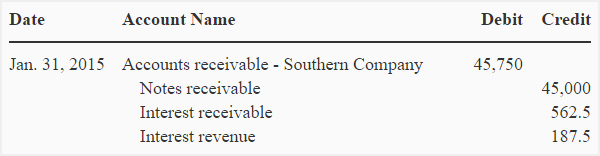

The above example illustrates the situation where maker duly makes the payment; but if the maker fails to make the payment at the date of maturity, the note is said to have been defaulted. A defaulted note is worthless. The amount due from the notes receivable is immediately transferred to its relevant accounts receivable. Suppose, in the above example, if Southern Company fails to make the payment against $45,750 note, the Western Company will make the following journal entry to record this default:

Notice that the interest has also been included in the accounts receivable because it is as valid a claim as the principle amount on the note itself.

Leave a comment