Difference between standards and budgets

There is not much difference between standards and budgets. In cost and management accounting, the term “standard cost” means the budgeted cost of one unit of product and the term budget means the cost of whole budgeted production.

For example, Excel Health Care company uses standard costing system. The finished product of the company is a sachet that contains health supplement for the people of all ages.

The expected or standard materials cost to produce one sachet is $5 and the budgeted production for the next month is 1000 sachets. It means the standard cost of materials at Excel Health Care is $5 and the budgeted cost of material would be $5,000.

If standard direct labor cost of Excel Health Care is $3 and standard manufacturing overhead cost is $2, the standard unit cost may be calculated as follows:

The standard cost is $10 and budgeted cost is $10000 (1000 units × $10) for the next moth.

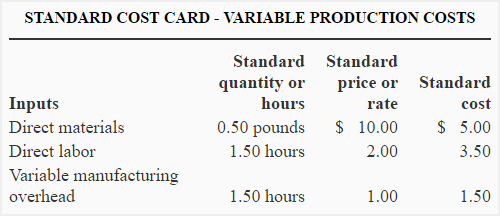

Standard costs for all cost elements (direct materials, direct labor and manufacturing overhead) are written on a document known as standard cost card. A standard cost card is prepared for every individual product. The proper form of standard cost card is as follows:

Leave a comment