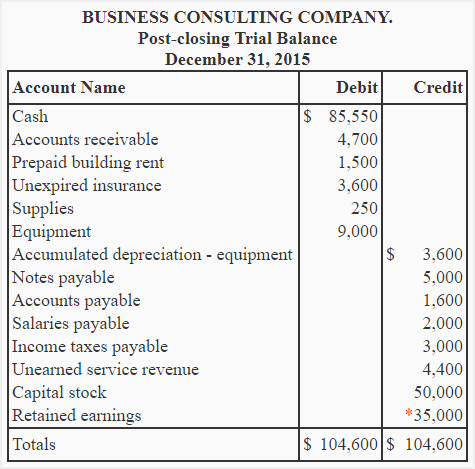

Post-closing trial balance

The post-closing trial balance (also known as after-closing trial balance) is the ninth and last step of accounting cycle which is prepared after making and posting all necessary closing entries to relevant ledger accounts. Since closing entries close all temporary ledger accounts, the post-closing trial balance consists of only permanent ledger accounts (i.e, balance sheet accounts). The purpose of preparing a post-closing trial balance is to assure that accounts are in balance and ready for recording transactions in the next accounting period.

Example

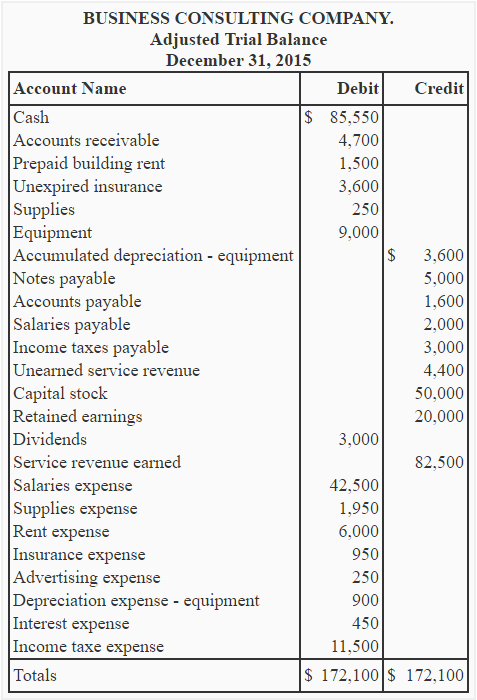

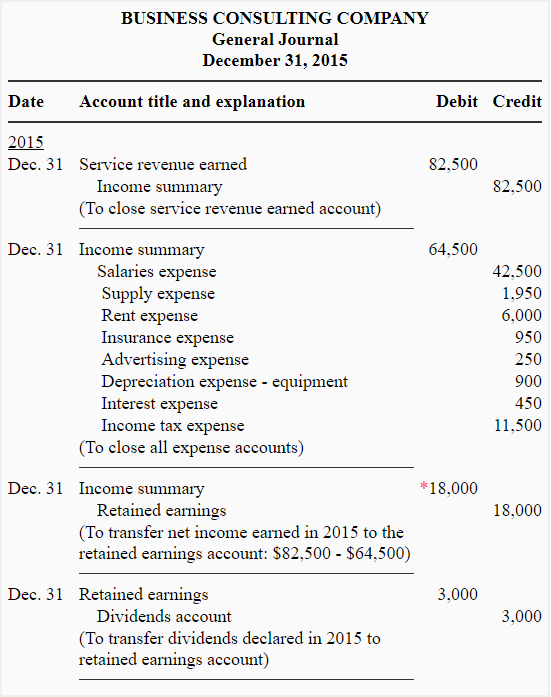

Adjusted trial balance and closing entries of Business Consulting Company are given below:

*$82,500 – $64,500

Required: Using the information from adjusted trial balance and closing entries given above, prepare post-closing trial balance of Business Consulting Company.

Solution

*Balance of retained earnings account has been updated as follows:

Retained earnings as per adjusted trial balance + Net income – Dividends

= $20,000 + $18,000 – $3,000

= $35,000

Notice that the post-closing trial balance prepared above lists only permanent or balance sheet accounts. The balances of all temporary accounts (i.e., revenue, expense, dividend and income summary accounts) have turned to zero because of the above mentioned closing entries. These temporary accounts have therefore not been listed in post-closing trial balance.

With the preparation of post-closing trial balance, the accounting cycle for an accounting period comes to its end. In the next accounting period, this cycle starts again with the first step i.e., preparation of journal entries.

The notes given are comprehensive and educative. Is there any site for these topics to be downloaded?